If you own a flat in the UK with a short lease and you want to sell, you are in a difficult position. Mortgage lenders pull back, estate agents hesitate to take the instruction, and every month that passes the lease gets shorter and the flat loses value. The situation is fixable, but the route you choose depends on your timeline, your budget, and how much certainty you need.

This guide sets out how to sell a short lease flat in the UK in 2026. We cover what counts as short, why these flats are hard to sell on the open market, your four realistic selling options, how to value the flat honestly, the decision between extending the lease first or selling as-is, the legal points you should not skip, and a timeline showing what to expect from each route. We write this as specialists who buy short lease flats every week, so the advice reflects what actually happens rather than what the textbooks suggest.

Whether you are in London, the South East, the Midlands or a regional city, the mechanics are the same. The buyer pool shrinks under 80 years, shrinks further under 70, and narrows to cash only under 60. Knowing where your flat sits on that curve is the first step.

What counts as a short lease?

A flat has a short lease when the remaining term is low enough that it materially affects value, mortgageability, or the cost of extension. In practice, four thresholds matter:

- Above 80 years: a long lease for most purposes. Mortgage lenders are comfortable, the flat sells on normal terms, and lease extension is cheaper because marriage value does not apply.

- 70 to 80 years: on the edge. Some buyers and lenders become cautious. You can usually still sell through an estate agent, but the ground is shifting under you. Below 80 years, marriage value becomes payable when extending.

- 60 to 70 years: short. Most mainstream mortgage lenders decline. The flat is effectively a cash or specialist-finance purchase. Agents will take the instruction but struggle to find buyers. Value drops 15 to 30 percent versus the long-lease equivalent.

- Under 60 years: very short. The mainstream mortgage market is closed. Extension premiums are substantial because marriage value compounds. Specialist cash buyers, auction investors, and the occasional cash buyer are the realistic pool. Discounts of 30 percent or more are common.

For a deeper look at what qualifies as short and why the 80-year line matters, see our guide on what is a short lease. If you want to see the depreciation curve visually, the lease length and property value chart maps value loss against lease length.

Why short lease flats are hard to sell on the open market

It helps to understand what is actually happening in the market before you pick a route. Four forces work against a normal sale:

Mortgage lenders pull back. Most high street lenders, including the major banks and building societies, require at least 70 to 85 years remaining at completion, with a further requirement that 25 to 50 years remain at the end of the mortgage term. The details vary by lender, but the practical effect is the same: around 90 percent of UK flat buyers use a mortgage, and almost all of them are out of the pool once the lease drops below 70 years. See our short leases and mortgages guide for lender-by-lender detail.

Buyer concerns compound. Even a cash buyer who could complete looks at a short lease flat and sees a to-do list. They know they will have to extend, which means legal costs, valuer fees, a premium, and possibly a Section 42 notice. They factor all of that into their offer, so even if a sale happens, the price reflects the total cost of making the flat normal again.

Marriage value adds to extension costs. Once the lease drops under 80 years, the freeholder is entitled to a share of the "marriage value", the uplift in value that comes from extending. This can add 30 to 70 percent to the extension premium depending on lease length. Reform is pending under the Leasehold and Freehold Reform Act, but at time of writing it is not yet in force. See marriage value explained for the mechanics.

Time works against you. Property on the open market takes months, not weeks. For a short lease flat, the typical marketing period is 6 to 12 months, sometimes longer. During that time, the lease shortens. A flat listed with 72 years might go under offer with 71, and complete with 70. That is not hypothetical; we see it in our valuations every month. For flats near the 80-year line, the difference between selling in month 2 versus month 10 can be thousands of pounds in price.

The impact on price is well documented. RICS relativity tables and market data suggest:

- 70 to 80 years remaining: typically a 5 to 15 percent reduction versus the equivalent long-lease flat

- 60 to 70 years remaining: typically 15 to 30 percent

- Under 60 years: often 30 percent or more

These ranges are indicative. Actual figures depend on location, flat type, condition, the freeholder's willingness, and current market conditions. For a proper figure, get a RICS-qualified valuation or speak to a specialist.

Your four realistic selling options

There are four realistic ways to sell a short lease flat. The right one depends on how quickly you need to complete, how much capital you can put up front, and how much risk you are willing to accept on the final price.

Option one: sell through an estate agent. Standard open market sale via Rightmove, Zoopla and a local agent. Can work for flats with 80+ years, or sometimes 70 to 80 if the rest of the proposition is strong. Below 70 years, most agents will be honest that it will be slow. Pros: widest market exposure, potential to achieve a higher price. Cons: long timeline, risk of sale falling through at mortgage stage, commission fees of 1 to 3 percent plus VAT, and the lease keeps shortening while the flat is marketed.

Option two: sell at auction. Traditional auction (Allsop, Savills, Barnard Marcus) or modern method auction. Attracts cash buyers and investors who actively look for short lease opportunities. Pros: defined timeline, contracts binding on the hammer falling (traditional auction), sale usually completes within 6 to 10 weeks. Cons: no guarantee the reserve is met, auction fees including entry fees and 2 to 3 percent commission, price can disappoint if bidding is thin, and the public guide-price history follows the flat if it fails to sell.

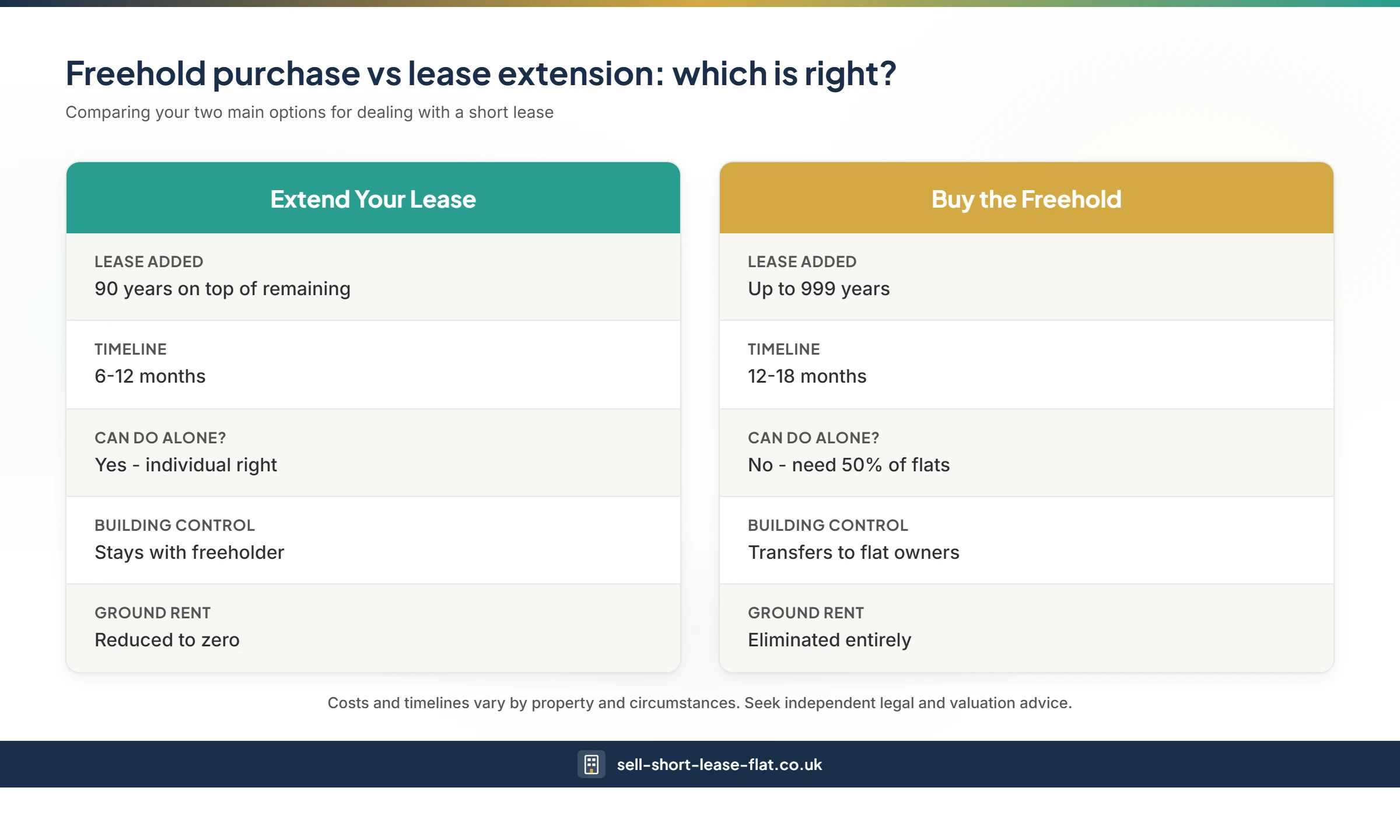

Option three: extend the lease first, then sell. Serve a Section 42 notice under the Leasehold Reform, Housing and Urban Development Act 1993, add 90 years to your current lease and reduce ground rent to a peppercorn, then sell the now-long-lease flat on normal terms. Pros: maximum sale price, widest buyer pool, access to mortgage-backed buyers. Cons: 6 to 12 months for a statutory extension, premium and professional fees typically £30,000 to £70,000 or more for inner London flats, you need to have owned the flat for at least two years, and you fund all of it up front.

Option four: sell directly to a specialist cash buyer. A specialist buyer (such as our service) makes a cash offer and purchases the flat as-is, handling the lease extension themselves after completion. Pros: no chain, no mortgage dependency, completion in 2 to 4 weeks, no fees to you, your solicitor costs covered, buys any lease length. Cons: the offer is below the flat's long-lease value because the buyer has to factor in the cost of the extension and their own margin.

For an in-depth comparison of these four routes including worked examples, read your selling options compared.

Getting a realistic valuation

A short lease flat has two values in play at the same time: what it would be worth with a long lease, and what it is actually worth with the lease you have today. Knowing both matters because every offer you receive reflects the gap between them.

The standard valuation approach works in three parts:

Start with the long-lease value. Look at recent sale prices for comparable flats in your building or postcode with 90+ year leases. Portals like Rightmove's sold price history and the Land Registry are your first stop. A local RICS surveyor can give a more precise figure.

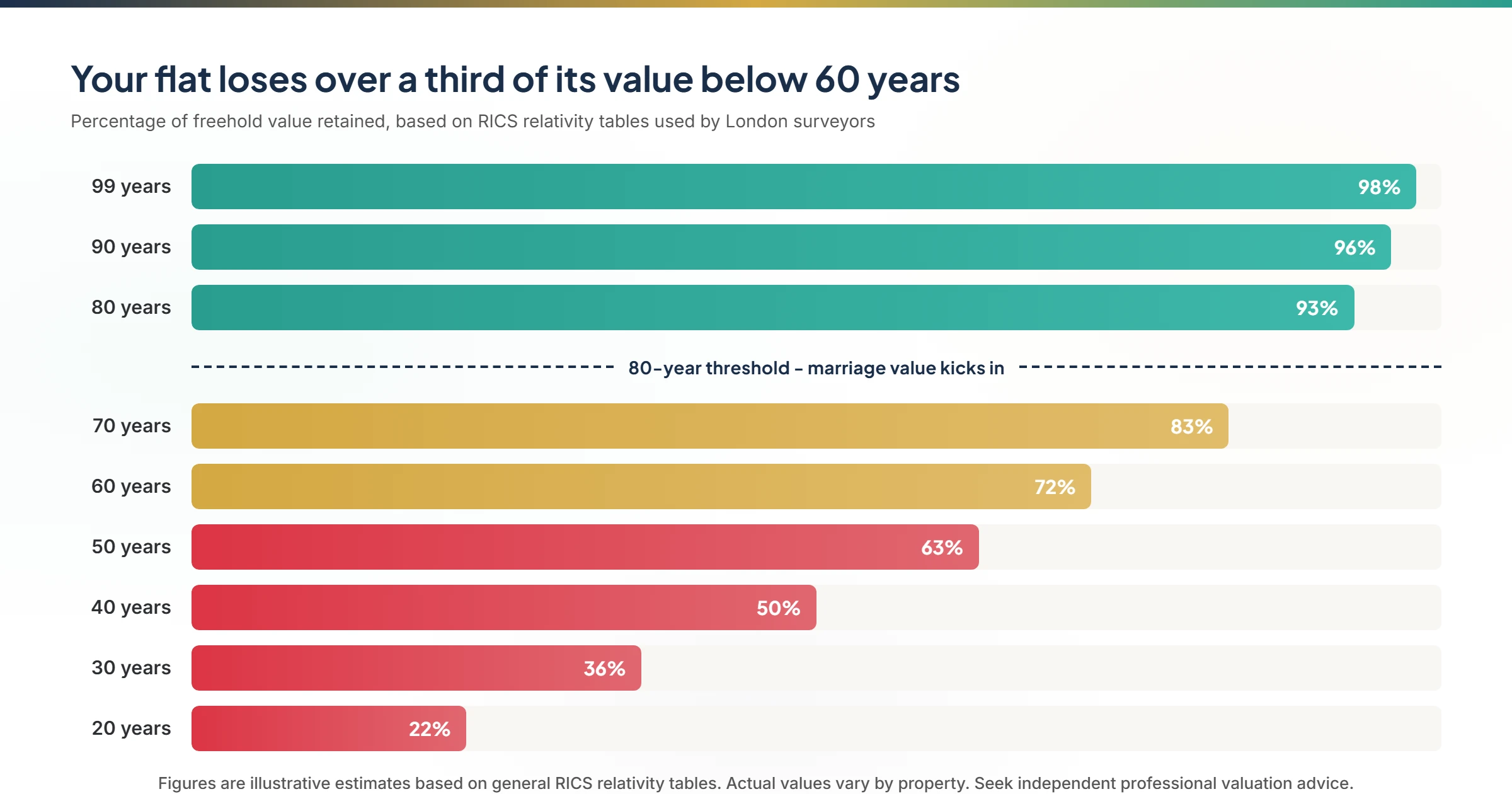

Apply a relativity percentage. RICS relativity tables (and proprietary variants used by surveyors) estimate what percentage of the long-lease value the flat is worth at the current lease length. Around 80 years, the figure is typically in the mid to high 90s. At 70 years, the low to mid 80s. At 60 years, roughly 72 to 78 percent. At 50 years, 60 to 68 percent. These are rough guides and vary by location and the specific relativity graph a surveyor uses.

Deduct the cost of extension. Any buyer who needs the lease extended to make the flat normal again will factor in the premium, their legal costs, surveyor fees, and the freeholder's reasonable costs. For a typical inner London flat with 60 years remaining, that total outlay can easily reach £40,000 to £60,000. For a regional flat on a lower base value, extension costs are lower but still material.

Worked example: a two-bedroom flat in a London borough worth £500,000 with a long lease. At 65 years, a relativity of around 76 percent gives a short-lease value of £380,000. A buyer who plans to extend estimates their total extension cost at £55,000. Their offer, before a margin for risk and holding costs, is around £325,000. Depending on how they price risk and the margin they need, the final offer might land between £300,000 and £325,000.

The lease extension calculator gives a starting estimate for extension premiums, though the only binding figure comes from a qualified valuer in a Section 42 valuation. Treat online calculators as ballpark indicators. All estimates should be confirmed by independent professional advice before you rely on them.

Lease extension versus sell as-is: the key decision

The single biggest financial decision you make is whether to extend the lease before selling or sell the flat as it stands. It is not a generic choice. The right answer depends on three numbers: how much cash you have now, how much time you have before you need the money, and how the arithmetic plays out at your specific lease length.

When extending first makes sense. You have enough cash (typically £35,000 to £70,000 or more for inner London, lower elsewhere). You can wait 12 to 18 months for the whole process. The flat is in a location and building where a long lease will attract mortgage buyers at a much higher price point. You have owned the flat for at least two years (a prerequisite for the statutory route). You are not in financial pressure, probate timelines, or divorce proceedings that require speed.

When selling as-is makes sense. You need to sell quickly. You cannot or do not want to fund the extension. The lease is very short (under 50 years) and extension premiums are significant. The flat has other issues (cladding, ground rent clauses, short section 20 consultations pending) that would complicate a normal sale even after extension. The arithmetic is genuinely close and certainty matters more to you than squeezing the top price.

A useful test: if you have 70 years or more, the cash to pay the premium, and a year to spare, extending first usually produces the better net result. If you have less than 60 years, limited cash, and need to complete within three months, selling as-is is almost always the right call. The middle range, 60 to 70 years with moderate cash, is where the decision is finely balanced and depends heavily on the specific flat.

For a head-to-head on the options, including whether buying the freehold is viable instead, see buying the freehold versus extending your lease.

Marriage value and the 80-year threshold

Marriage value is the single biggest reason 80 years is the hinge point for short leases. Under current law, when you extend a lease with fewer than 80 years remaining, the freeholder is entitled to 50 percent of the uplift in value that the extension creates. This is the marriage value. It can add tens of thousands of pounds to the premium.

Example: a flat with a 78-year lease is worth £295,000. With a 168-year lease it would be worth £310,000. The marriage value is £15,000, and the freeholder is entitled to half of that on top of the basic premium. Drop the lease to 68 years and the gap grows, and so does the marriage value share.

The Leasehold and Freehold Reform Act 2024 contains provisions to abolish marriage value and cap how premiums are calculated. Royal Assent was granted in May 2024. However, the provisions require secondary legislation to come into force, and at the time of writing that secondary legislation has not been laid. Several freeholder groups have also challenged the Act in the courts, and those proceedings are ongoing. See our news piece on freeholders taking reform to the Court of Appeal for the current state of play.

The practical point for sellers: do not wait for reform. The provisions may arrive in 2027, 2028, or later, and in the meantime your lease is getting shorter. If you have 79 years and wait for marriage value abolition, you may have 74 years when it lands, and the mortgage market will be harder to access regardless of the marriage value position. Read marriage value explained for the full mechanics.

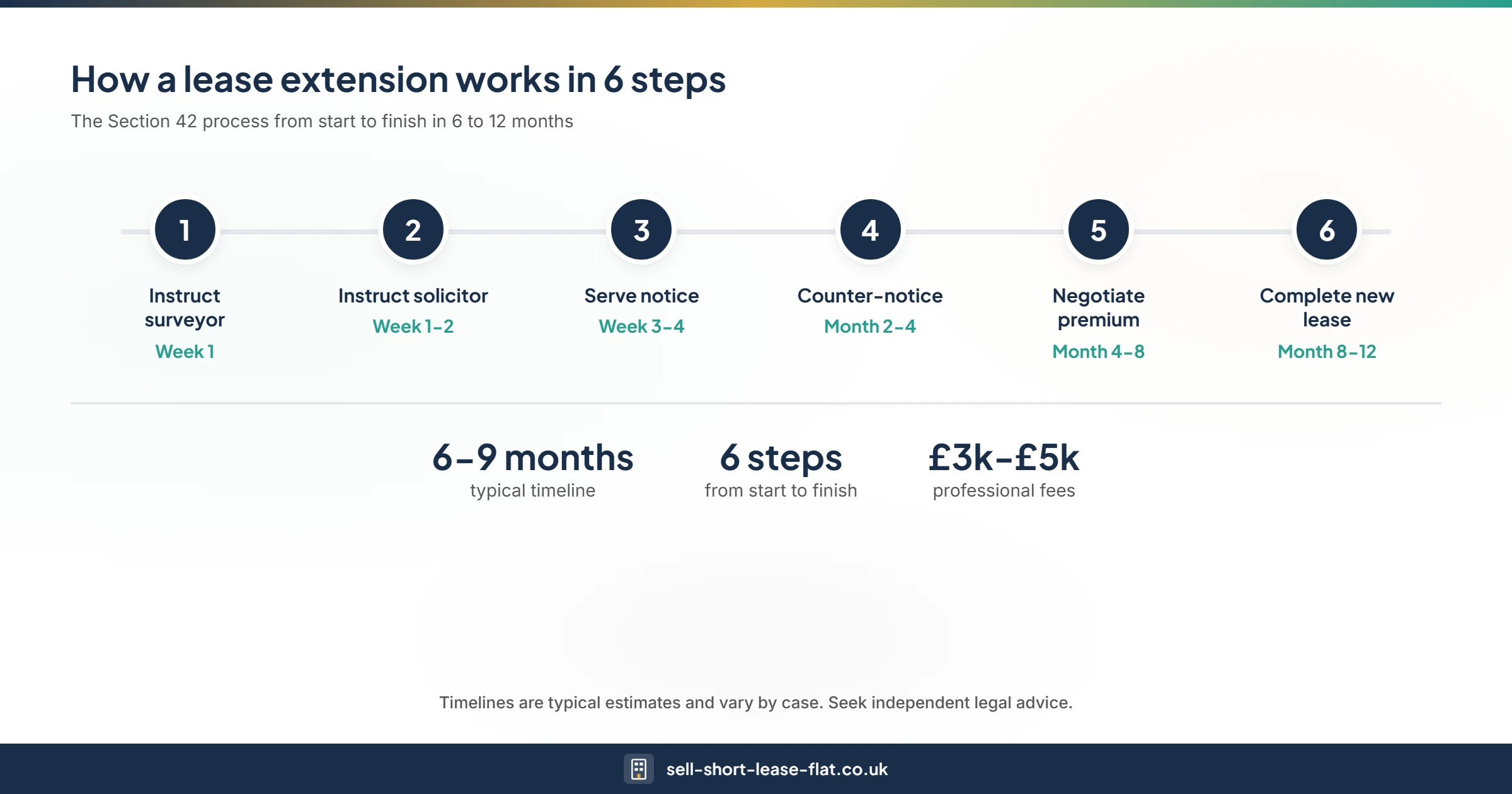

Section 42 and the Leasehold Reform Act

If you do decide to extend, the statutory route is a Section 42 notice. This is a formal notice served on the freeholder under the 1993 Act. It triggers a process in which:

- You serve notice claiming a statutory extension (90 years added to the current lease, ground rent reduced to a peppercorn).

- The freeholder responds with a counter-notice, usually within two months, stating their premium and terms.

- You and the freeholder negotiate, with a fallback to the First-tier Tribunal (Property Chamber) if you cannot agree.

- Once terms are agreed, solicitors complete the new lease. The whole process typically takes 6 to 12 months.

You must have owned the flat for at least two years to use the Section 42 route. If you are within that window, you can still pursue an informal extension with the freeholder but you lose the statutory protections, including the fixed extension term and the ground rent reduction.

For a step-by-step guide, see Section 42 notice guide. For an overview of which reform provisions are actually in force versus still pending, see our news coverage of which provisions of the Leasehold Reform Act are now active.

Mortgage and buyer constraints

The mortgage market is the single biggest constraint on who will buy your flat. Lender rules are conservative and they have tightened over the past decade. A typical mainstream lender applies two tests:

- Minimum lease at completion: usually 70 to 85 years. Halifax, Nationwide and Santander typically want 85 years; HSBC and Barclays are more flexible at 70 to 80.

- Minimum lease remaining at the end of the mortgage term: usually 25 to 50 years. So on a 25-year mortgage with a 70-year lease today, you would have 45 years left at the end of the term, which sits inside most lender rules. On a 30-year mortgage with a 70-year lease, you would have 40 years left at the end, which fails some lenders.

Specialist lenders (Together, Vida, Kensington, Kent Reliance) will lend on shorter leases but at higher interest rates and lower loan-to-value ratios. For leases under 60 years, the commercial mortgage market is effectively the only route for a financed buyer, and those deals are rare.

That is why cash buyers dominate the short lease market. Buy-to-let investors, specialist property buyers like us, auction investors, and occasionally downsizing homeowners paying outright make up the pool. When you price the flat, you price for that pool, not for the whole market. For a lender-by-lender breakdown, read short leases and mortgages.

Legal and tax considerations

A short lease sale is a normal conveyancing transaction with a few extra points to watch.

Pick a solicitor who does leasehold work regularly. A generalist residential conveyancer can handle the paperwork, but a solicitor experienced in leasehold will spot issues that matter to buyers, such as ground rent escalation clauses, section 20 consultations in progress, reserved sinking fund positions, or freeholder disputes. Buyers or their solicitors will raise these as enquiries and a practised leasehold solicitor will move the sale along faster.

Capital gains tax may apply. If the flat has been your main residence the whole time you owned it, private residence relief usually covers any gain. If the flat has been let out, was inherited, or you owned it alongside another property, CGT may apply on the gain above the annual exempt amount. The rules are not simple, and rates depend on your overall income. Do not rely on rules of thumb; speak to an accountant or tax adviser. For an overview of the issues, see capital gains tax when selling a short lease flat. Tax figures in any guide are illustrative only and never a substitute for professional advice.

Disclose what you know. The standard TA6 and TA7 seller disclosure forms ask about disputes, planned works, and lease compliance. Answer honestly. Undisclosed known issues surface at buyer-solicitor enquiry stage and kill deals at the last minute.

Get independent professional advice. This guide is written to help you understand the landscape. It is not legal, financial, or tax advice. Before you sign anything, speak to a RICS-qualified valuer, a leasehold-experienced solicitor, and where relevant a tax adviser.

Timeline: what to expect

Here is how the four routes typically play out week by week:

Cash buyer route:

- Week 1: Submit details, receive valuation, review offer

- Week 2: Accept offer, instruct solicitor, buyer runs legal searches

- Week 3: Enquiries raised and answered

- Week 4: Exchange and complete, funds in your account

Total: 2 to 4 weeks is typical. We have completed inside 10 working days when circumstances demand.

Auction route:

- Weeks 1 to 3: Instruct auction house, prepare legal pack, set reserve and guide price

- Weeks 4 to 5: Pre-auction marketing

- Week 6: Auction day. If sold, buyer pays 10 percent deposit

- Weeks 7 to 10: Completion within 28 days (traditional) or 56 days (modern method)

Total: 6 to 10 weeks if the reserve is met. Nothing if it is not.

Estate agent route:

- Weeks 1 to 2: Agent valuation, photography, listing

- Weeks 3 to 24+: Viewings, offers, negotiation. Short lease flats regularly sit at this stage for months

- After acceptance: 8 to 12 weeks of conveyancing. Risk of sale falling through at mortgage stage

Total: 6 to 12 months is normal. Longer is not unusual.

Extend then sell route:

- Months 1 to 2: Instruct valuer, serve Section 42 notice

- Months 2 to 8: Freeholder counter-notice, negotiation, tribunal if needed

- Months 8 to 12: Complete lease extension

- Months 12 to 18: Sell on the open market with a long lease

Total: 12 to 18 months, plus substantial upfront capital.

Frequently asked questions

How fast can I sell a short lease flat?

Selling to a specialist cash buyer typically completes in 2 to 4 weeks. Auctions take 6 to 10 weeks. Estate agent sales take 6 to 12 months or longer. Extending first adds 6 to 12 months to whichever route you choose.

Can I sell a flat with under 60 years left on the lease?

Yes, but your buyer pool is narrow. Mainstream mortgage lenders decline, so realistic buyers are cash purchasers, buy-to-let investors with specialist finance, and specialist short lease buyers. Expect an offer around 60 to 70 percent of the flat's long-lease value.

Do I need to extend the lease before selling?

Not always. Extending first usually produces the highest sale price, but it requires capital, time, and at least two years of ownership for the statutory route. If you need to complete quickly, cannot fund the premium, or the lease is very short, selling as-is to a specialist buyer is usually the more practical outcome.

What is the minimum lease a buyer will accept?

Mainstream mortgage lenders commonly want 70 to 85 years at completion with 25 to 50 years remaining at the end of the mortgage term. Specialist lenders will go shorter at higher rates. Cash buyers, including our service, will consider any lease length.

Are specialist cash buyers regulated?

Credible buyers are members of The Property Ombudsman or a similar redress scheme, registered with the ICO, and have a registered company number. Check Companies House and the Ombudsman directory before proceeding, and always take independent legal advice before signing.

Will the Leasehold and Freehold Reform Act make my flat easier to sell?

Eventually, yes. Most of the seller-relevant provisions, including marriage value abolition, require secondary legislation which is not yet in force and which is being challenged in court. Your lease depreciates while you wait, so basing a sell-now decision on reform timing is rarely worthwhile.

Do you buy short lease flats outside London?

Yes. Our deepest expertise is London but we buy across England and Wales, from the Home Counties and the South East commuter belt to major regional cities and coastal towns. Contact us with your postcode and lease details for a valuation.

What fees will I pay to sell to a cash buyer?

When selling to us, there is no commission, no marketing cost, and your reasonable solicitor fees are covered. The offer is the amount you receive. This is the main practical difference versus an estate agent sale (1 to 3 percent plus VAT commission) or auction (entry fee plus commission).

Next steps

If you want a figure for your specific flat, request a free valuation or call us on 020 7183 3022. We will give you an honest assessment of your options, even if the best route is not selling to us. For related reading, our guides hub has the deeper detail on each of the topics above.

This guide is written for general information. It is not legal, financial, or tax advice. Figures and timelines are indicative and vary by flat, location, and current market conditions. Always take independent professional advice before making a decision.