This calculator estimates the cost of extending a residential lease on an English or Welsh flat under the statutory route, which is by far the most common path for short lease owners. It is built on the same Gerald Eve 1996 graph of relativities that surveyors and the First-tier Tribunal Property Chamber rely on when valuing lease extensions, with marriage value applied where the remaining term falls below 80 years. Below the widget we walk through how the numbers are produced, what changes at the key thresholds, three worked examples, and how the Leasehold and Freehold Reform Act 2024 will eventually reshape the maths.

How the calculation works

Three components combine to make up an extension premium. The first is the capitalised value of the ground rent the freeholder gives up over the remaining term of the existing lease. The second is the reversion value, which is the present-day value of the freeholder receiving the flat back at the end of the lease, discounted using a deferment rate set by tribunal precedent. The third, where the remaining lease has fallen below 80 years, is marriage value, which is the uplift in flat value released by extending and which the legislation currently splits 50/50 between leaseholder and freeholder.

The calculator uses the Gerald Eve 1996 graph of relativities, which expresses short lease value as a percentage of the long lease value at each remaining year. The figures it produces are deliberately conservative and align with the relativity evidence most commonly accepted by the First-tier Tribunal. For a deeper dive into the methodology and where it can go wrong, see our guide to marriage value.

What changes under 80, 70 and 60 years

The cost of extending does not rise smoothly. It steps up at three thresholds that are well established in valuation practice and lender criteria.

80 years is the first cliff. Above this line the freeholder is not entitled to any marriage value. Below it, half of the uplift the extension releases goes to the freeholder. For a typical London flat, that single change adds £10,000 to £30,000 to the premium and grows quickly as the lease shortens further. Extending while you are still above 80 years is materially cheaper than waiting and is the single most cost-effective move available to a long-lease owner whose term is drifting down.

70 years is the mortgage threshold most mainstream high-street lenders apply. Below 70 years a typical flat will not be eligible for a residential mortgage with Halifax, Santander, NatWest, Barclays or HSBC, narrowing the buyer pool sharply if you ever want to sell without extending. Specialist lenders will go lower but at significantly higher rates and stricter terms.

60 years is where the depreciation curve gets steep. The reversion value the freeholder is giving up grows much faster, and the discount sellers face widens from around 15-30 per cent of long-lease value to 30 per cent or more. See our guide on how a short lease affects flat value for the full curve.

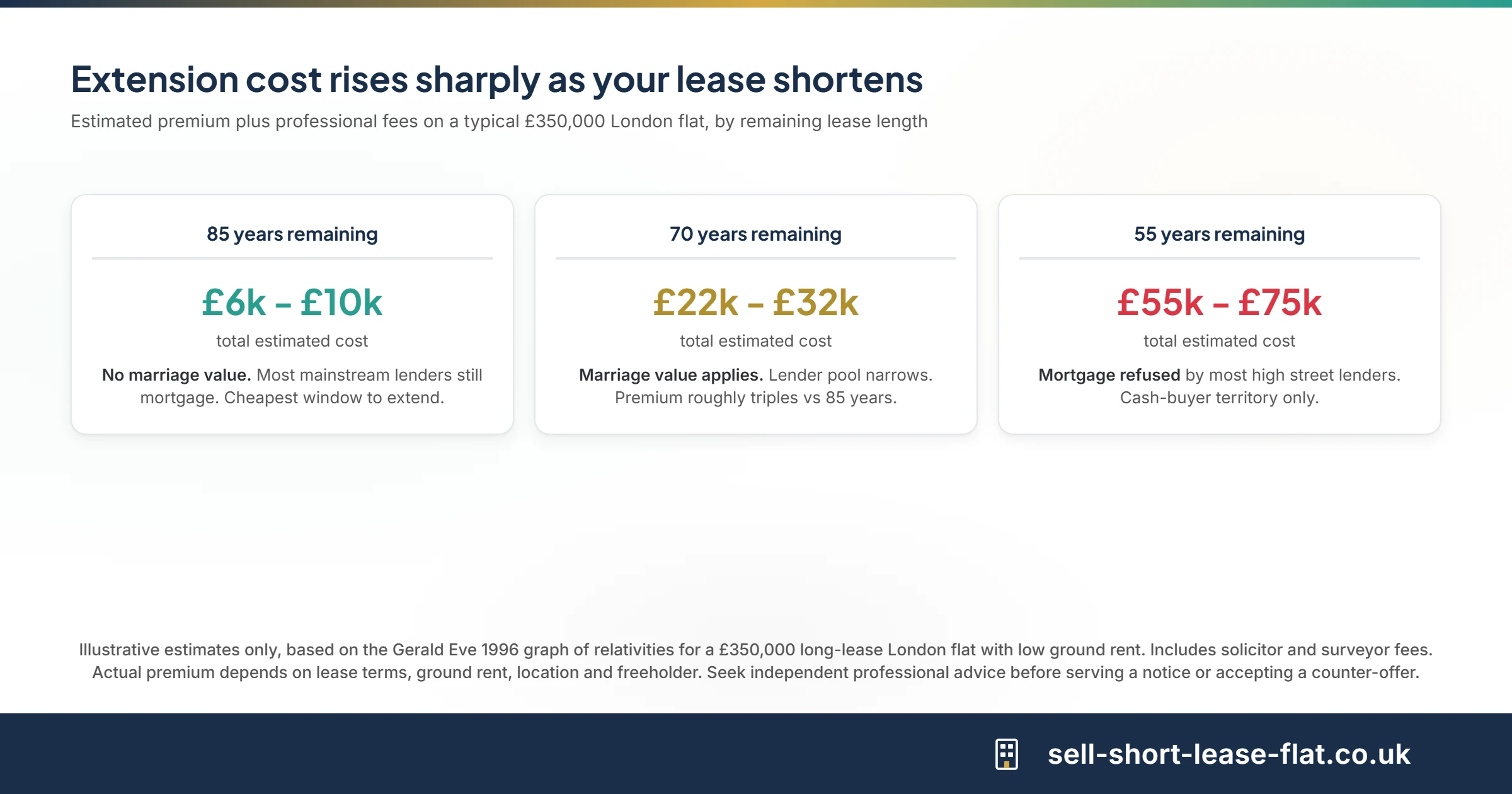

Three worked examples

The same £350,000 long-lease London flat produces very different extension costs depending on where the remaining term sits. All figures below are illustrative estimates based on the Gerald Eve relativity graph with low ground rent and standard deferment and capitalisation rates.

- 85 years remaining. Premium typically £4,000 to £7,000. Plus around £2,300 of solicitor and surveyor fees. Total cost roughly £6,000 to £10,000. No marriage value. This is the cheapest extension window and any long-lease owner with a flat drifting toward 80 should be looking seriously at locking this in.

- 70 years remaining. Premium typically £18,000 to £27,000. Add the same £2,300 of professional fees, plus the freeholder's reasonable legal and surveyor costs. Total around £22,000 to £32,000. Marriage value now applies. The premium has roughly tripled compared with the 85-year example for what looks superficially like a modest reduction in remaining term.

- 55 years remaining. Premium typically £50,000 to £70,000. Total cost including fees and freeholder costs roughly £55,000 to £75,000. Marriage value is now a large share of the bill, and the reversion the freeholder is giving up has also grown. Most mainstream lenders will refuse a mortgage on a flat with 55 years left, so the realistic buyer pool is cash buyers and investors.

Professional fees and freeholder costs

The premium itself is only part of the total bill. A statutory lease extension also requires a specialist leasehold solicitor and a leasehold-experienced surveyor, both of whom are necessary because the work is technical and the consequences of errors are expensive. Indicative ranges in 2026:

- Solicitor: £1,000 to £2,000 plus VAT for drafting and serving the Section 42 notice and handling the conveyancing.

- Surveyor: £500 to £1,000 plus VAT for the initial valuation report. Tribunal-level evidence costs more.

- Freeholder's reasonable costs: the leaseholder is required to cover the freeholder's legal and surveyor costs to a reasonable level. Typically £1,500 to £3,000 in standard cases, more if the freeholder instructs city firms.

These figures are the practical reason the calculator's "total cost" output sits noticeably above the bare premium. They also tip the maths in favour of acting early: if you are going to incur the fixed professional costs anyway, doing it while your lease is still above 80 years avoids paying them on top of marriage value as well.

The Section 42 statutory route versus an informal extension

There are two ways to extend a lease and they are not equivalent. The statutory route, started by serving a Section 42 notice under the Leasehold Reform, Housing and Urban Development Act 1993, gives the leaseholder a 90-year extension on top of the existing term, reduces the ground rent to a peppercorn, and locks in the valuation date for the premium. Once the notice is served, the freeholder cannot refuse the extension; they can only dispute the premium, and any dispute is resolved by the First-tier Tribunal Property Chamber. This is the route used in almost every case where the leaseholder needs certainty.

An informal extension is a negotiated agreement directly with the freeholder without serving a Section 42 notice. It can be faster and cheaper to set up, but it offers no statutory protection on price, term length or ground rent treatment. Freeholders sometimes offer informal extensions on shorter terms with a retained ground rent, which can be a poor long-term outcome compared with the statutory route. For most short lease owners, the statutory route is the better choice. Our Section 42 notice guide walks through the process step by step. If you would prefer ongoing one-to-one help, our lease extension advice page sets out where to get it.

How the Leasehold and Freehold Reform Act will change the maths

The Leasehold and Freehold Reform Act 2024 (LAFRA) overhauls the statutory extension regime. The headline changes that affect the premium are:

- Marriage value is abolished. The 50 per cent share currently paid to the freeholder on extensions of leases below 80 years is removed entirely. For a 65-year lease on a typical London flat this saves £20,000 to £40,000.

- The statutory term jumps from 90 to 990 years. The extension is effectively permanent and removes the need ever to extend again.

- Ground rent reduced to a peppercorn. Aligns with current statutory practice, made explicit in the new methodology.

- Standardised valuation methodology with prescribed deferment and capitalisation rates, reducing the scope for tribunal dispute.

None of these provisions are in force as of May 2026. The marriage value commencement order has not been laid, and the Government has indicated that the headline reforms are not expected to take effect before late 2028. We track the timeline in detail in our King's Speech briefing, our piece on Pennycook's 29 April timeline update, and our marriage value delay explainer. For the underlying Act, see our guide to the Leasehold and Freehold Reform Act 2024.

The strategic question is whether waiting for LAFRA commencement is worth more than the cost of continued lease depreciation in the meantime. For owners well above 80 years, no, because they are not paying marriage value anyway. For owners below 80 years with no need to sell soon, it can be worth considering, but the 2028 implementation window is now formally a floor rather than a ceiling and the lease keeps ticking down in the meantime.

Mortgage implications for short leases

A high extension premium is one half of the cost story. The other half is what happens to the flat's mortgageability if you do not extend. Most mainstream UK lenders require a lease of at least 70 years remaining at the start of the mortgage, with a few setting the bar at 80. Once a flat falls below 70 years, the realistic buyer pool drops by roughly 80 to 90 per cent and is dominated by cash buyers and investors. Specialist lenders will mortgage flats with fewer years remaining but at premium rates and tighter loan-to-value caps.

The practical implication for sellers is that the extension calculator's premium output should be read alongside the discount you would otherwise need to accept on an unextended sale. In many short lease cases the premium is materially less than the open-market discount, which is the textbook reason to extend before listing. Our guide to short leases and mortgages sets out the current lender thresholds in detail.

Sell or extend? When the calculator output tips one way

The calculator gives you three numbers: the premium, the total cost including fees, and the resulting uplift in flat value. The rough decision rule is straightforward. If the uplift is materially larger than the total cost, extending is the better financial outcome. If they are close, or if the cost is higher than the uplift, the sums favour selling without extending and letting a cash buyer pay the price discount instead. In practice the answer also depends on cashflow, time available, and whether you actually want to keep the flat at all.

If extending does not stack up, or if you simply want to move quickly without the conveyancing burden of an extension, we buy short lease flats for cash across the UK with no fees and no chain. Compare the routes in our guides to selling options compared, buying the freehold versus extending, and our full step-by-step guide to selling a short lease flat.

Frequently asked questions

How accurate is a lease extension calculator?

Online lease extension calculators give an order-of-magnitude estimate based on the Gerald Eve 1996 graph of relativities. They are accurate enough for budgeting but should not be relied on for serving a Section 42 notice. For that you need a formal valuation from a specialist surveyor familiar with your local tribunal evidence.

What is marriage value and when does it apply?

Marriage value is the increase in flat value released by extending the lease, half of which is currently payable to the freeholder. It only applies when the lease falls below 80 years remaining. Above 80 years the premium covers the capitalised ground rent and the deferred reversion only. See our full marriage value explainer.

Why does the lease extension cost rise sharply below 80 years?

Two things happen at once. Marriage value becomes payable for the first time, adding tens of thousands to the premium. And the reversion value the freeholder gives up grows materially as the lease shortens. The combined effect is why the 80-year threshold is treated as a cliff edge rather than a gradient.

How long does a lease extension take?

A statutory extension via a Section 42 notice typically takes six to twelve months from notice to completion. Informal extensions negotiated directly with the freeholder can be quicker but offer no statutory protection on price or terms. Tribunal disputes can extend the timeline by a further six months or more.

What is a Section 42 notice?

A Section 42 notice is the formal statutory request to extend a lease under the Leasehold Reform, Housing and Urban Development Act 1993. Serving it preserves the leaseholder's right to a 90-year extension on top of the existing term, with ground rent reduced to a peppercorn, and locks in the valuation date for the premium calculation. Our Section 42 notice guide walks through the process.

Will the Leasehold and Freehold Reform Act make my extension cheaper?

Yes for leases below 80 years, because marriage value is being abolished. The reform also extends the statutory term to 990 years and adjusts the valuation methodology. None of these provisions are in force as of May 2026, with the Government working to a 2028 implementation window.

Can the freeholder refuse a statutory lease extension?

Not where the leaseholder meets the qualifying criteria. A qualifying tenant of a long lease has a statutory right to extend, and the freeholder cannot refuse. They can dispute the premium, in which case the matter goes to the First-tier Tribunal Property Chamber for determination.

What are deferment and capitalisation rates?

The deferment rate is the discount rate used to convert the freeholder's future reversion into present value. The capitalisation rate does the same for the ground rent income stream. Both are set by tribunal precedent and vary by region. In prime London they are typically 5 to 5.5 per cent. The lower the rate, the higher the premium.

Do I need a specialist solicitor and surveyor for a lease extension?

Yes for a statutory extension. The legal and valuation work is highly technical and a general high street solicitor will rarely have the experience. Expect to pay £1,000 to £2,000 for the solicitor and £500 to £1,000 for the surveyor, plus the freeholder's reasonable costs which the leaseholder is required to cover.

Is it ever cheaper to buy the freehold instead of extending the lease?

Sometimes, particularly in small blocks of two to four flats where the leaseholders can act collectively. Collective enfranchisement gives leaseholders control of ground rent, service charges and forfeiture, and can be cheaper per flat than serving individual Section 42 notices. See our buying the freehold versus extending guide for the trade-offs.