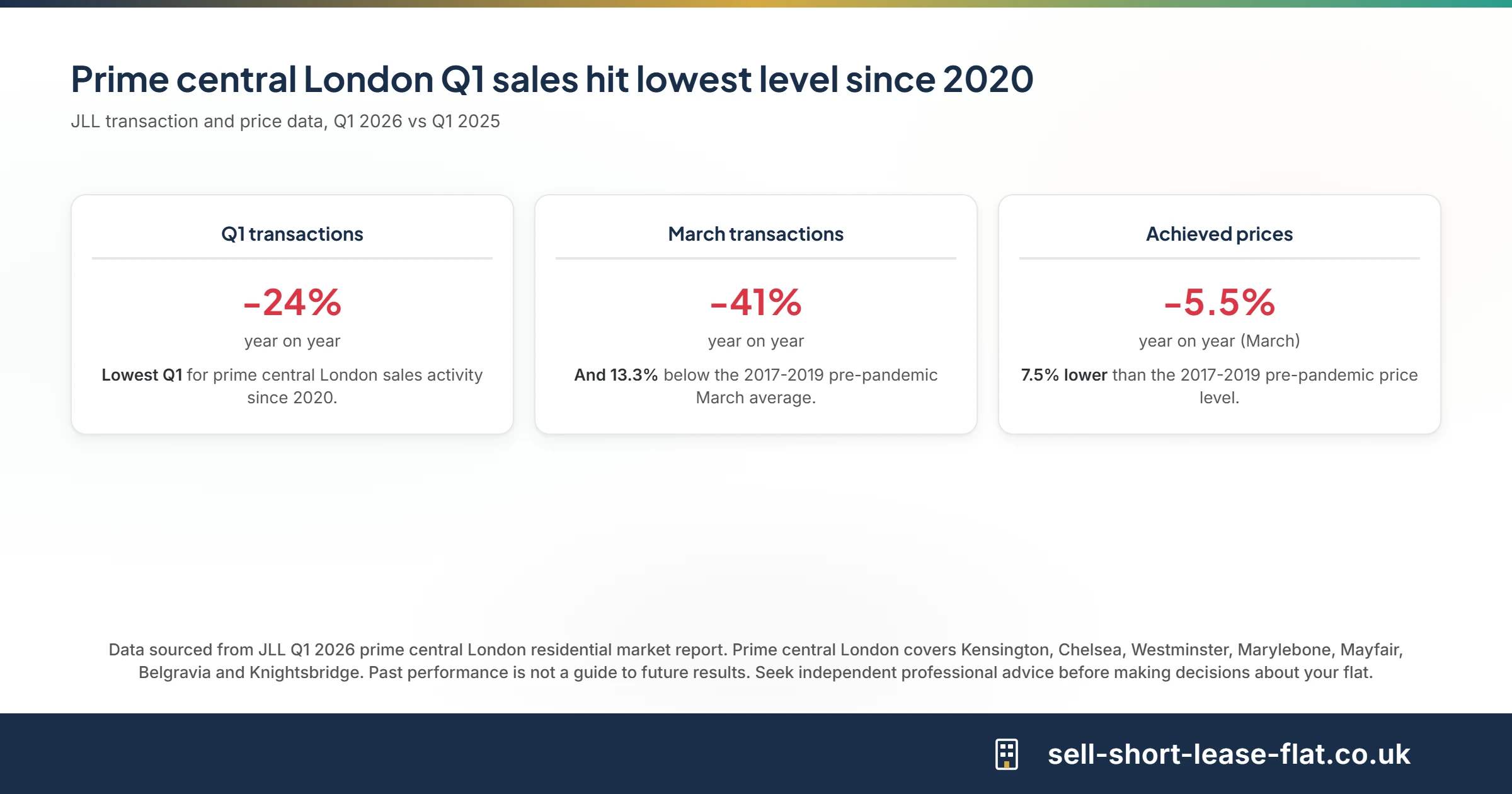

JLL's Q1 2026 prime central London residential market report, published in the past fortnight, makes for uncomfortable reading. Sales transactions in the prime central postcodes fell 24 per cent year on year, the lowest first-quarter level since 2020. March alone was 41 per cent down on March 2025, and 13.3 per cent below the average for March across 2017 to 2019. Achieved sold prices in March came in 5.5 per cent lower than a year earlier and 7.5 per cent below the same pre-pandemic baseline.

For owners of short lease flats in Kensington, Chelsea, Westminster, Marylebone, Mayfair, Belgravia and Knightsbridge, this is the part of the market backdrop that matters most. Prime central London is the postcode pool where most of the country's short lease flats sit, because it is where the historic period leasehold housing stock is concentrated. A wider market slump in the prime postcodes compounds the lease-length discount, and the data behind the headline numbers is worth unpacking.

What the JLL data actually shows

JLL's data is built on Land Registry completions plus its own off-market intelligence in the prime central postcodes. Three numbers are worth keeping in mind:

- Q1 transactions down 24 per cent. This is the headline. Q1 2026 prime central London volumes were the lowest first quarter since the early-pandemic shutdown in 2020. Even the famously slow Q1 2024 came in higher than this one.

- March alone down 41 per cent. The year-on-year fall is exaggerated by an unusually strong March 2025, but March 2026 was still 13.3 per cent below the 2017-2019 March average. The slowdown is structural, not just a base-effect.

- Achieved prices down 5.5 per cent year on year. This is the actual transaction price, not the asking price. Sold prices in prime central London are now 7.5 per cent below the pre-pandemic level, before adjusting for inflation. Adjusted for CPI, the real-terms fall is significantly larger.

Stock has not collapsed alongside transactions. The number of homes for sale at end of March was 13.8 per cent higher than a year earlier, although still below the peak reached in September 2025. More flats sitting on the market with fewer buyers willing to commit is the worst possible combination if you are trying to sell.

Why this hits short lease flats harder

A slump in prime central London is not the same problem for every flat. For a long-lease, mortgageable flat in a renovated building, fewer buyers means a slower sale and a probable price reduction. Painful, but recoverable. For a short lease flat, the slump layers on top of an existing discount and shrinks the buyer pool from two directions at once.

Most mainstream lenders will not write a mortgage on a flat with fewer than 70 years remaining on the lease, with several drawing the line at 80 years. Short lease flats in the 70-80 year band typically sell at a 5-15 per cent discount to long-lease comparables. Between 60 and 70 years the discount widens to 15-30 per cent, and below 60 years it crosses 30 per cent plus. Our guide on how a short lease affects your flat's value goes into the numbers.

That discount is calculated against the long-lease price. If the long-lease price itself is falling, the cash you end up with after the discount falls in lockstep. A flat priced at £1.2m on a long lease last year, sitting on a 67-year lease, was already looking at a 15-30 per cent discount. If the long-lease comparable now clears at £1.13m, the discount applies to a smaller number. The lease length and the slump combine multiplicatively, not additively.

The other factor is time. Short lease flats already take longer to sell than long-lease equivalents - typically 6 to 9 months in a normal market, often longer. In a slump, that timeline stretches further. Every month spent on the market is a month closer to the next critical lease-length threshold, and the lease keeps depreciating even when the market is flat.

The marriage value question, refreshed

The reform context matters here too. The Leasehold and Freehold Reform Act 2024 promised to abolish marriage value on leases under 80 years, but the commencement orders are still outstanding. The Government has indicated the headline provisions are not expected to take effect before late 2028. Our breakdown of which parts of LAFRA are in force covers the current position.

For a prime central London short lease owner, the slump and the reform delay are now intertwined. Waiting for the abolition of marriage value could save tens of thousands on a future extension premium, but the cost of waiting is paid in two ways: continued lease depreciation, and exposure to a falling market in the postcodes where most prime short leases sit. There is no clean answer that works for every flat. The right call depends on lease length, holding cost, and how soon you actually need the proceeds.

What sellers in prime central London should think about

A few practical reads on the current data:

- Price to the comparable, not the memory. If your last formal valuation predates the slump, it is probably stale. Recent achieved prices, not asking prices, are the only number that matters when you are setting a level.

- Account for time on market. A 6-month listing in a falling market means your lease has shortened by six months on top of any price reduction. Build that into your planning. Our guide on selling options compared walks through the trade-offs of estate agent, auction, extend-first and direct sale.

- Look at borough-level dynamics. Prime central is not uniform. Kensington and Chelsea and Westminster are showing the steepest declines in the JLL series; some adjoining boroughs are holding up better.

- Be honest about the buyer pool. With mortgage-dependent buyers thinner on the ground, the realistic short lease buyer is a cash buyer or an investor. Both groups know exactly what discount they expect. Setting expectations early reduces the chance of an offer collapse at the conveyancing stage.

Where to read more

JLL's Q1 prime central London commentary is summarised in trade press including Property Week and Estate Agent Today. For the wider London picture, our piece on the two-speed flat-versus-house market covers the ONS data behind the headline.

If you would like a clear, honest valuation that reflects current prime central London comparables and your specific lease length, get in touch. We specialise in short lease flats across London and the rest of the UK, and there is no obligation either way. Our step-by-step guide to selling a short lease flat covers the full process end to end.